Introducing MTSOS: Trade the Entire Bittensor Subnet Economy

MegaTAO is launching MTSOS, the MegaTAO Sum-of-Subnets index perpetual. It is the first derivatives instrument that gives traders direct leveraged exposure to the entire Bittensor subnet economy in a single position. The market runs on a custom EMA oracle we built in-house to smooth out distortions in the underlying on-chain price data. This post explains what MTSOS is, why we built the oracle the way we did, and how it works.

What Is MTSOS?

Every Alpha market on MegaTAO tracks one subnet. MTSOS tracks all of them at once. The index price is the sum of all Alpha token prices, denominated in TAO, fed through a 7-day exponential moving average oracle we built specifically for this market.

The value proposition is straightforward. If you think the Bittensor ecosystem is growing but you don't want to pick which subnets win, you long MTSOS. If you think it contracts, you short it. No subnet research required, no concentration risk in a single market.

- Long MTSOS: bullish on the Bittensor subnet economy as a whole

- Short MTSOS: hedging broad Alpha exposure or bearish on subnet valuations overall

- Pair trades: long a specific subnet Alpha market, short MTSOS to isolate idiosyncratic subnet performance

For users new to MegaTAO or to Bittensor in general, MTSOS is also the natural starting point. It diversifies subnet selection risk automatically, making it a cleaner first exposure to Alpha-denominated perps before getting into individual markets.

Why We Needed a New Oracle

Bittensor's EVM layer exposes a precompile at address 0x0808 that returns the sum of all Alpha token prices as a single on-chain value via getSumAlphaPrice(). It is convenient and entirely on-chain, but when we started observing the data we noticed a problem.

The spot value is not always stable. During our pre-launch monitoring, we captured this datapoint at block 7710784 on March 9, 2026:

That 1.7579 TAO value (a 35% spike above the surrounding readings) is not a display artifact. We confirmed it by calling the precompile directly on the archive node at that exact block. It is a genuine single-block distortion in the on-chain data source itself.

The problem with using raw spot as an oracle: A single-block spike of this magnitude, if used directly as a perp price feed, creates an immediate liquidation event for any leveraged long whose liquidation price falls below the spike level, or a windfall for any short with a closing order in that block. Neither outcome reflects real market conditions. This kind of manipulation or data glitch would be catastrophic for a live derivatives market.

Why EMA: Smoothing Out Single-Block Distortions

Exponential moving averages are a standard tool in oracle design precisely because they dampen single-period outliers. An EMA weights recent observations but distributes that weight continuously over a decay window. A one-block spike contributes only a tiny fraction of its value to the EMA. By the next block, its influence is already shrinking.

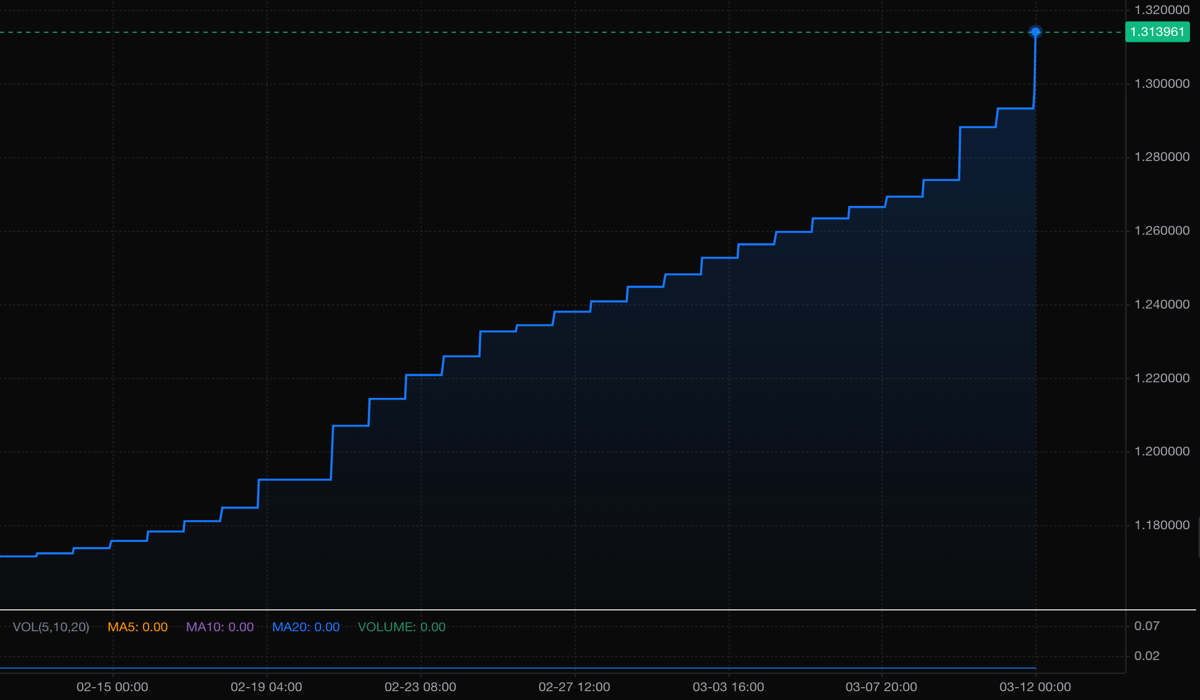

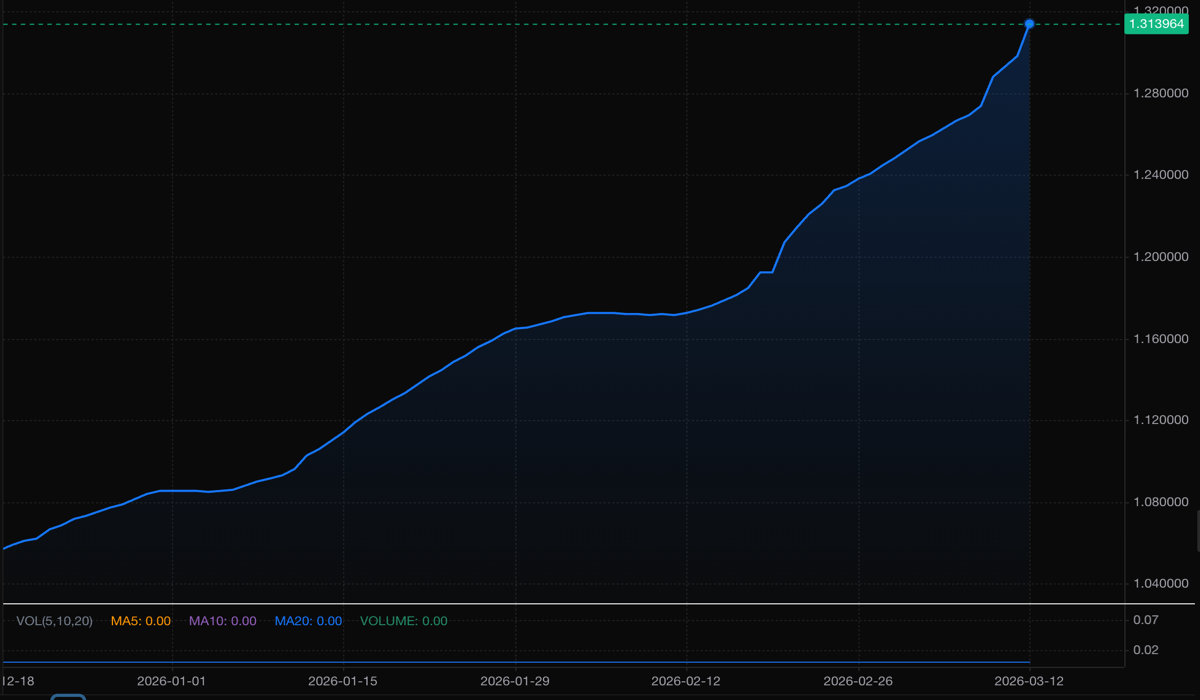

The contrast between the raw spot price and the EMA oracle is visible across both the past month and the past three months of data.

Last Month (Feb 10 – Mar 10)

Last 3 Months (Dec 17 – Mar 10)

The EMA Formula

We built a dedicated IndexPriceOracle contract that wraps the raw precompile output in a 7-day EMA. The oracle uses a time-weighted EMA, where the decay is continuous rather than block-discrete. Each call to update the EMA computes:

newEma = (spot × elapsed + prevEma × 604800) / (elapsed + 604800)Where elapsed is the number of seconds since the last update, and 604800 is 7 days expressed in seconds (the EMA decay period).

What this means in practice:

- Whenever the EMA is updated once per hour (elapsed ≈ 3600s), the spot price contributes approximately 0.6% of the new EMA value. The remaining 99.4% comes from the previous EMA.

- A single-block spike like the 1.7579 reading above, even if it persisted for a full hour, would shift the EMA by roughly 0.003 TAO. That is a 0.2% move on a 1.30 TAO index. Completely harmless for a derivatives market.

- A genuine, sustained move in the underlying index, where spot stays elevated or depressed across many consecutive updates, does propagate into the EMA over time. The oracle is not a lag machine; it is a spike filter.

Example: With the EMA initialized at 1.2993 TAO on March 9 and the subnet economy appreciating ~3.3% over the following 24 hours, the EMA tracks to ~1.3093 TAO while spot sits at ~1.3429 TAO, a 2.6% gap. This is expected behavior. The 7-day decay means the EMA will converge to spot gradually if the move is sustained, rather than jumping on a single reading.

Leverage on Day 1: Up to 5x

MTSOS launches with up to 5x leverage available from day one. The EMA oracle provides a stability layer on top of that: because the price feed is smoothed, the abrupt short-term swings that cause cascading liquidations in raw-spot markets are structurally reduced. Traders get the leverage they need; the protocol manages the oracle-level noise.

Liquidation Parameters

A position is liquidated when its equity (margin plus unrealized PnL) falls below 10% of notional. At 5x leverage the initial margin is 20% of notional, so you have a 10-percentage-point buffer before liquidation.

At 5x, a position is liquidated when the index moves 10% against it. Monitor your positions actively. The EMA oracle reduces the risk of sudden oracle-driven liquidations, but it does not protect against real index moves.

Risk note: Higher leverage means a smaller move wipes your margin. Factor in funding rates and trading fees, which reduce your effective buffer further. At 5x with a 0.25% open fee and a 0.25% close fee, you are already starting 0.5% in the hole against your liquidation buffer. Size positions accordingly.

Summary

- MTSOS is a perpetual futures market on the sum of all Bittensor Alpha token prices, giving exposure to the entire subnet economy in one position

- The price oracle is a 7-day time-weighted EMA wrapped around the on-chain

getSumAlphaPrice()precompile, built specifically to handle the single-block distortions we observed in raw spot data - EMA formula:

(spot × elapsed + prevEma × 604800) / (elapsed + 604800)with a 7-day (604800s) decay period - Up to 5x leverage is available from day one

- Liquidation threshold: 10% of notional; at 5x leverage, a position liquidates after a 10% adverse move

When Does It Launch?

MTSOS is expected to go live next week. We will announce the exact date on X (Twitter) and in Discord before it opens. Once live, you will be able to trade it at megatao.io/trade.

Leveraged trading involves significant risk. You can lose your entire margin. Only trade with capital you can afford to lose.